If you’re a seasoned credit card churner, or simply someone who has applied for lots of credit cards, you’ve probably heard of the 5/24 rule.

It’s Chase’s internal credit card rule that automatically disqualifies you from ALL their credit cards if you’ve opened five other cards in the past 24 months.

So if you opened two Amex cards, two Citi cards, and a Discover card over the past two years, Chase won’t approve you for one of their cards.

It doesn’t matter if you’ve got excellent credit, no Chase credit cards, and no balances on existing cards.

They’ll simply deny you on the grounds that you opened too many new cards recently.

Capital One Credit Card Application Rules

- Chase’s 5/24 rule automatically denies applicants if they’ve opened five or more personal credit card accounts (from any issuer) in the past 24 months

- Capital One doesn’t have an official 5/24 rule like Chase, but anecdotal evidence suggests they consider recent credit card applications

- I was denied a Capital One Spark 2X Miles Business Card at exactly 5/24, with the denial reason citing “too many new accounts,” hinting at a similar threshold

- This was despite a strong credit profile otherwise (high credit scores, low balances, good credit mix, no late payments ever)

- Capital One also limits customers to two personal credit cards at a time (business cards excluded from this limit) with a minimum 6-month waiting period between Capital One card approvals

Chase’s 5/24 rule is probably the most well-known credit card rule out there. Mainly because it’s a hard stop.

If you opened five new cards in the past 24 months, you’re out. There is no rebuttal. There is no reconsideration.

You’ve effectively wasted a credit inquiry (and some time filling out a credit card application).

Interestingly, you can’t even open a business card from Chase, such as Ink Business Cash, if you’ve got five new personal credit cards on your credit report in the past 24 months.

However, the business cards themselves don’t count toward 5/24 status.

Anyway, that brings me to my particular situation. I am currently at exactly 5/24.

I’ve opened five new personal credit cards over the past 24 months, including:

- Amex Gold

- Citi Premier

- Venture X

- Amex Platinum

- Chase Sapphire Preferred

I’ve been on a roll lately, grabbing sign-up bonuses and looking for new ones. But knowing I was at 5/24, I wanted to apply for a business credit card.

That way the new business card wouldn’t contribute to my 5/24 status, and the oldest of my five new cards would fall off soon.

In fact, in late March 2023 I’ll be back to 4/24, which opens the door to Chase credit cards again.

Capital One Spark 2X Miles Business Card Is Offering 50,000 Miles

I did some comparison shopping and discovered the Capital One “Spark 2X Miles” card.

It piqued my interest for several reasons. One, it was a business card, meaning no contribution to 5/24 status.

Second, it offered 50,000 miles after spending $4,500, and 2X miles on every purchase along the way (plus 5X on hotels and rental cars booked via Capital One Travel).

And third, a $95 annual fee, which is waived the first year. All in all, a good way to snag about 60,000 miles that can be transferred to airline/hotel partners.

It’s not amazing by any means, but the $0 annual fee in year one and the relatively easy minimum spend makes it a strong contender.

As noted, it’s also a business card, which narrowed the field significantly.

So without thinking too much, I went for it. I only have one Capital One card at the moment, the Venture X.

And I knew my credit scores were excellent, and existing balances low.

Despite being at 5/24, I only opened two new personal cards in the past 365 days.

Nothing excessive, a relatively clean credit profile (in my opinion).

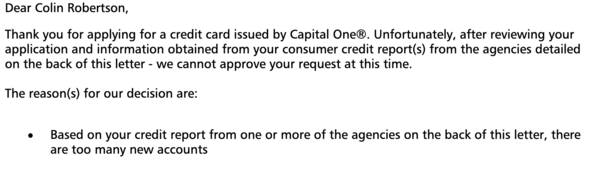

We Are Unable to Approve Your Application

I filled out the application for the Spark 2X Miles and hit submit. A few tense seconds and boom, not approved. Ugh.

Minutes later, I received an email that stated, “Colin, unfortunately we were unable to approve your application at this time.”

“We know you’re disappointed. To help you understand why, we’ve explained the reason for this decision in a letter or email that you’ll receive within 10 days.”

Not sure if it made me feel better that they knew I was disappointed.

Anyway, the next day I got the “letter” via email. Specifically, an “Adverse Action Letter.” Talk about dramatic.

It was pretty black and white: “Based on your credit report from one or more of the agencies on the back of this letter, there are too many new accounts”

It also listed my credit score of 780, which was sourced from Experian, using a credit score range of 300-850.

Okay, so that cleared a few things up. I had excellent credit, so that wasn’t the issue. And there weren’t any address, name, or business name mismatches.

The reason was simple – too many new accounts. And the only accounts they’re talking about are personal credit card accounts.

Is There a Capital One 5/24 Rule?

I just so happened to be exactly at 5/24, which is Chase’s rule and grounds for automatic denial.

Could it be that Capital One credit card application rules also include a 5/24 rule, which is maybe more clandestine or lesser known?

It certainly wouldn’t surprise me, and does make me wonder if I would have been approved for Spark 2X Miles at 4/24.

Capital One supposedly has other unwritten credit card rules, including a maximum of two personal Capital One credit cards at any given time (biz cards don’t count toward this total).

And a minimum six month waiting period between Capital One approvals, which seems reasonable.

Anyway, if you’re at or above 5/24, you may want to think twice before applying for a Capital One credit card, including both personal and business cards.

(photo: Bill Selak)

- Make Sure You Have a Premium Chase Credit Card so You Can Transfer Points! - February 21, 2025

- Do Capital One Credit Cards Have a 5/24 Rule Too? - February 23, 2023

- Quickly See the Many Ways You Can Use American Express Membership Rewards Points - February 21, 2023