Chase credit cards are very popular. Mainly because they earn Ultimate Rewards, which can be transferred to hotel and airline partners. However, only certain Chase credit cards have this feature. Many Chase cards do not earn transferable Ultimate Rewards. If they don’t, your only redemption options are cash back (100 points = $1) or gift… Continue reading Make Sure You Have a Premium Chase Credit Card so You Can Transfer Points!

Category: Credit Help and Tips

Master your credit card and credit score, all in one convenient place.

Do Capital One Credit Cards Have a 5/24 Rule Too?

If you’re a seasoned credit card churner, or simply someone who has applied for lots of credit cards, you’ve probably heard of the 5/24 rule. It’s Chase’s internal credit card rule that automatically disqualifies you from ALL their credit cards if you’ve opened five other cards in the past 24 months. So if you opened… Continue reading Do Capital One Credit Cards Have a 5/24 Rule Too?

Quickly See the Many Ways You Can Use American Express Membership Rewards Points

I recently applied for the American Express Gold card because it was offering a whopping 90k sign-up bonus. Specifically, Amex offered me 90,000 Membership Rewards points if I spent a piddly $4,000 in the first six months from account opening. Roughly $667 in spending per month, which is about as good as it gets, especially… Continue reading Quickly See the Many Ways You Can Use American Express Membership Rewards Points

Best Gas Credit Cards – Earn Up to 8X Points!

Let’s take a look at the best gas credit cards to maximize your points or cash back. Gas prices saw some relief lately, but that’s sure to change as the year goes on. And per usual, gas prices will likely surge as summer arrives. In fact, GasBuddy warned of $7 a gallon gas in places… Continue reading Best Gas Credit Cards – Earn Up to 8X Points!

Citi Premier Card Categories: Earn 3X on Gas, Groceries, and More

I wanted to do a simple post that focused solely on the Citi Premier Card categories. Why? Because I have the card in my wallet and constantly forget what it offers. But I know it comes with a lot of good stuff. So if nothing else, this will serve as a good reminder and personal… Continue reading Citi Premier Card Categories: Earn 3X on Gas, Groceries, and More

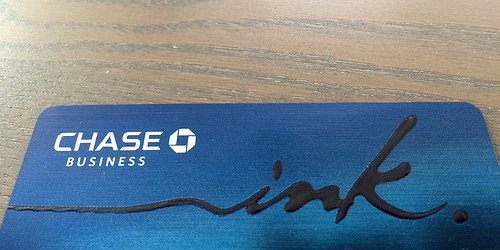

Yes, It’s Possible to Get Two Chase Ink Cards and Earn Two Separate Monster Bonuses

Some of the best credit card sign-up bonuses in existence are tied to the Chase Ink business credit cards. At last glance, you earn up to 100,000 points from Ink Business Preferred. And it only has a $95 annual fee. Take that Amex Platinum and your $695 annual fee. But there are two even better… Continue reading Yes, It’s Possible to Get Two Chase Ink Cards and Earn Two Separate Monster Bonuses

What Is Credit Card Churning? And Should You Take Part?

When you think of the word “churning,” what’s the first word that comes to mind? For me, it was “butter.” As in butter churn. But in the payment world there’s a newer and certainly riskier version, known as “credit card churning.” And it’s got nothing to do with butter. In fact, it has a lot… Continue reading What Is Credit Card Churning? And Should You Take Part?

Two Things to Do When You Open and Close a Credit Card

Whether you’re a credit noob, or a seasoned pro, there are two important things you should do every time you open and close a credit card. I thought of these things after I opened a slew of new credit cards to earn a bunch of awesome sign-up bonuses. If you’re also churning and burning, you… Continue reading Two Things to Do When You Open and Close a Credit Card

The Black American Express Credit Card Really Exists, But Is Kinda Weak

Ah the Black American Express Card, such a legend in the credit card world. But is it any good? Credit cards don’t typically fall into the category of pop-culture, nor do they usually garner much attention aside from their basic functionality. But one credit card has mystified and amazed consumers and the general public for… Continue reading The Black American Express Credit Card Really Exists, But Is Kinda Weak

Credit Card Minimum Spend: 10+ Ways to Earn That Big Bonus

Credit card Q&A: “How to meet credit card minimum spend?” There are always lucrative credit card sign-up bonuses available. But in many cases, you’ve got to spend an awful lot of money to get rewarded. If you just got approved for the Amex Platinum, but don’t know how you’ll spend $6,000, read on… For some… Continue reading Credit Card Minimum Spend: 10+ Ways to Earn That Big Bonus